There has been a good deal written about the IRS's threatened revocation of the tax exemption of All Saints Episcopal Church because of an anti-war sermon delivered the Sunday before the 2004 Presidential election. Anyone interested in the topic can found links to a good deal of the commentary at

TaxProf.

Earlier in the week,

Linda Beale reviewed the the IRS letter concerning the review, the church's response, and the sermon itself, as well as a November 13, 2005 sermon about the IRS issue. She concluded:

It is clear that the sermon mentioned specific political candidates by name and discussed specific policies and proposals forwarded by those candidates. It includes some negative statements about both Kerry and Bush, but it could be read to condemn many of Bush's policies and, implicitly, Bush's candidacy. Thus . . . it may well have crossed over the line drawn for tax exempt organizations.

I have given some thought to some of the broader policy issues posed by the audit and the response.

First, what is a partisan political statement or sermon? Certainly, there are sermons which most of us would agree are partisan (

e.g., Vote for the ________ Ticket (fill in your party of choice) because they are the party of the Lord.). However, beyond these easy questions (which the Pasadena sermon reveals not to be easy at all), there are many more difficult questions.

In the recent (non-partisan) Dover School Board election, evangelical churches and church leaders campaigned hard for the pro-ID candidates. And, of course, none other than the leader of the (501(c)(3), I think) 700 Club, Pat Robertson, promised (threatened?) Divine retribution on the citizenry of Dover for rejecting this particular "scientific" theory. Was the activity of the evangelical churches in favor of ID non-partisan simply because the pro and con candidates did not wear the "standard" party labels?

Going one step further, what happens when church leaders support some overriding goal (anti-pornography, anti-abortion, etc.) and the identifiably political candidates in support of those particular goals tend to be concentrated in one party or the other? Is "Vote for the Anti-Abortion Candidates" any less partisan than "Vote for Republicans" when all, or almost all, anti-abortion candidates are Republican candidates?

Needless to say, church activism in politics has a long lineage. Should African-American churches in the '50's and '60's been denied tax exempt status because of their leadership role in the civil rights movement? The anti-Vietnam movement later? The abolitionist movement 100 years before? (Ok, I know that this was before the income tax, but allow me my example.)

Politics need not always be intertwined with religious or moral issues, but frequently that is the case. I cannot comment on the minister in question, but I would suspect that his involvment in favor of John Kerry (actually, it seems, more in opposition to George Bush) was less problematic than the position of the Roman Catholic Church threatening to withhold the right to receive communion to political leaders who did not toe the line on the Church's position on abortion.

By their nature, Churches and the clergy involve themselves in politics, even if not always in an explicitly partisan manner. The issue is really one of line drawing, unless one wants to revoke tax exempt status for churches entirely. The line drawing process comes with its own set of problems, namely excessive entanglement with (or, perhaps more correctly here, against) religion.

The inevitability of some degree of entanglement has lead to calls to entirely do away with the charitable deduction for contributions to churches. However, this doesn't resolve the problem, it only moves the goal posts. If, for instance, we denied the charitable deduction for contributions to churches, tricky questions would begin to pop up: Is the contribution to a church-sponsored hospital or day school, a contribution to the church itself? What about a contribution to a college? Should Notre Dame or Yeshiva University be treated differently than a seminary?

Finally, it has been suggested that there not be any tax incentives to make charitable contributions. This could radically diminish the total amount of charitable giving.

A CBO study in 2002,

Effects of Allowing Nonitemizers to Deduct Charitable Contributions, found that:

[R]recent research suggests that the price elasticity of contributions by itemizers is more likely to be in the range of -0.4 to -0.8. If those estimates more accurately reflect taxpayer behavior, then a 10 percent decrease in the tax price would increase itemizers' contributions by between 4 percent and 8 percent.

Similarly, the estate tax has a positive effect on charitable giving. In testimony submitted to the Senate Committee on Finance Subcommittee on Social Security and Family Policy, in September of this year, William G. Gale of the Brookings Institution summarized studies on the effect of estate tax repeal on charitable giving as follows:

[A] variety of different kinds of research implies that estate tax repeal would reduce charitable bequests by between 22 and 37 percent, or between $3.6 billion and $6 billion per year. Previous studies are consistent with this finding, and also imply that repeal would reduce giving during life by a similar magnitude in dollar terms. To put this in perspective, a reduction in annual charitable donations in life and at death of $10 billion due to estate tax repeal represents a 5 percent decline in overall charitable giving and implies that, each year, the nonprofit sector would lose resources equivalent to the total grants currently made by the largest 110 foundations in the United States.

(Mr. Gale's testimony and some of the studies he relied upon can be found

here.)

On the whole, I'm prepared to continue to muddle along with our current system of classification. (I am not certain whether the "deduction" method should be replaced with a "tax credit" method, but that's a discussion for another day.) I think that, on the whole, the charitable contribution deduction serves an important purpose. Specifically, it contributes to the heterogeneity of our society. Thus, the government might cut off funding for certain types of genetic research, but the charitable contribution deduction provides a subsidy for what is, in effect, an alternative decision. (Please note: The issue is not whether one is for or against any particular form of genetic research. The issue is whether, as a society, it is in our best interest to have a tax subsidy that is contra to the majority decision on this and other issues.)

By way of example, I am strongly opposed to current attempts to insert religion, via ID, into the public school system. However, I do not oppose tax deductions to support foundations that do research into the validity of ID. (The concept of doing research on a hypothesis that is, by definition, not subject to refutation is somewhat oxymoronic, but so what.)

I also believe that religious organizations should stay out of politics. But I think that this is a principle that is easy to assert in the abstract, but difficult, if not impossible, to apply with consistency to actual cases.

Perhaps the best that we can hope for is that our application of the principle will be consistently inconsistent. That is, when religious organizations are audited for violations of the political involvement prohibitions, only the more extreme and persistent violations are met with serious penalties. We should turn a blind eye to trivial violations and the targets of audits attacking "exteme and persistent violations," taken as a whole, should be politically and religiously ecumenical.

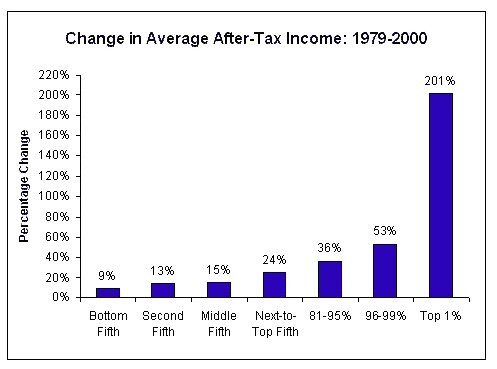

(Click to see a larger image.)

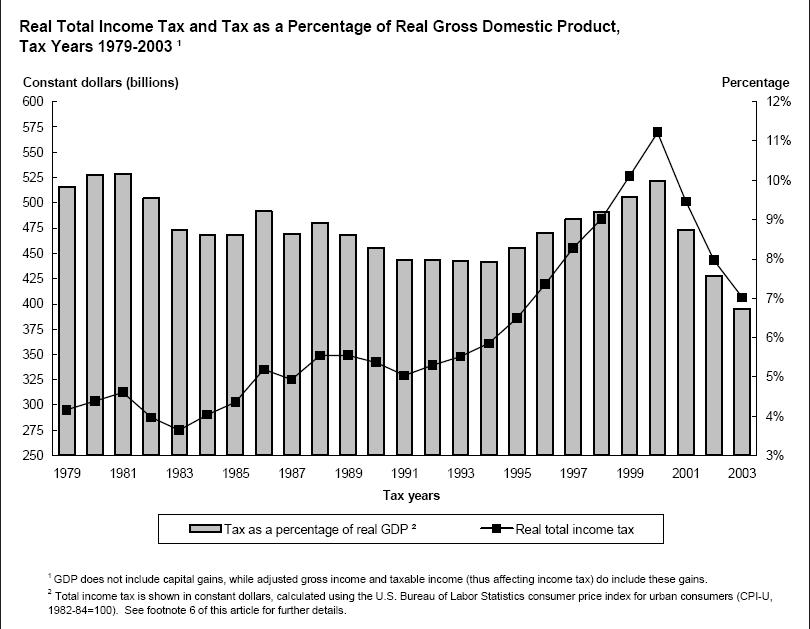

(Click to see a larger image.)

{kind=link}