The TF discussion was triggered by the appearance in public web access of a CRS report, Tax Expenditures: Trends and Critiques. (Why CRS reports remain a sort of public policy samizdat is beyond me. The report in question had actually been posted by TaxProf two weeks ago, but only this week became widely available via Open CRS. But that's a rant for another day.) Tax expenditures are "those revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability."

A good deal of the Tax Foundation's criticism is well founded. For instance, the posting states that:

Because tax preferences are less visible to voters than direct spending programs, they reduce the transparency of the nation's fiscal system. That's bad policy because—as we've learned from recent debate about problems with congressional "earmarking" — lack of fiscal transparency inevitably promotes wasteful spending, shielding ineffective programs from the cleansing power of public scrutiny and budgetary daylight.Recently, Linda Beale commented on a hearing held by:

[T]he Subcommittee on Federal Financial Management, Government Information, and International Security of the Senate Committee on Homeland Security and Governmental Affairs. . . . The hearing was titled "Deconstructing the Tax Code: Uncollected Taxes and Issues of Transparency." The hearing was "to examine uncollected taxes and issues of transparency relating to deconstructing the tax code, focusing on the 2006 updated estimate of the tax gap by the IRS, examine IRS efforts to close the tax gap as well as legislative solutions to increase taxpayer compliance, and explore the transparency of the tax code."(Link omitted.)

She concludes by saying that:

Any discussion of tax expenditures should result in greater transparency, not to the misleading ploys evident in the FY 2005 budget [where the reduction of tax rates on dividends from 35% to 15% was not defined by the Bush Administration as a tax expenditure]. Further, Congress should take care that discussions of tax expenditures do not act merely as an entree to renewed discussion of further revenue reductions rather than a genuine effort to make relevant tax information more accessible to ordinary Americans.It is here that the Tax Foundation comments miss the mark. Their posting states that:

[E]very additional tax expenditure carves out a portion of the nation's income tax base, forcing up tax rates to compensate. And as any economist will testify, higher marginal tax rates aren't bad simply because they make taxpayers "pay more." They're bad because they reduce the efficiency of the complex web of plans, contracts and relationships we call "the economy."(Some links omitted and emphasis added.)

Economists teach that the "deadweight losses" of taxes—that is, the pure economic waste that occurs as a side-effect of every tax—rise as the square of the tax rate. Here's what that means. If tax expenditures erode half the nation's tax base, and tax rates are doubled to raise the same revenue, the economic costs of the tax system don't simply double as well. They rise by four times in those markets that remain in the tax base.

The first paragraph in the TF posting is completely correct. The second paragraph is not.

The first link that I have left in goes to a Wikipedia entry that merely defines and discusses the concept of "deadweight loss." The second link goes to a Wikipedia entry that discusses the "Economics of Taxing a Good." But, in dealing with the question of whether or not to increase or decrease income taxes it is simply wrong to assume that all taxes create the same deadweight effect. Brad DeLong addressed this issue in January, 2005:

Now there are two analytically distinct claims there at the end of the first paragraph I quote, the first of which--for which I have a good deal of sympathy--is that our system of taxing income from capital has in all likelihood been very costly in terms of deadweight losses imposed on the economy when measured against the revenue raised and the progressivity gainedAll taxes have some deadweight effect. But to assume that the deadweight effect of all taxes is the square of the tax rate in all cases is to fall into the fallacy that all tax cuts will pay for themselves.

The second claim, however, is the problem. The second claim is the old supply-side b.s.: that the growth the tax cuts will unleash means that the tax cuts would more than pay for themselves.

If I were writing about that second claim, I would not say that "most economists typically find this line of argument questionable." I would say that an overwhelming majority of economists find this claim ludicrous.

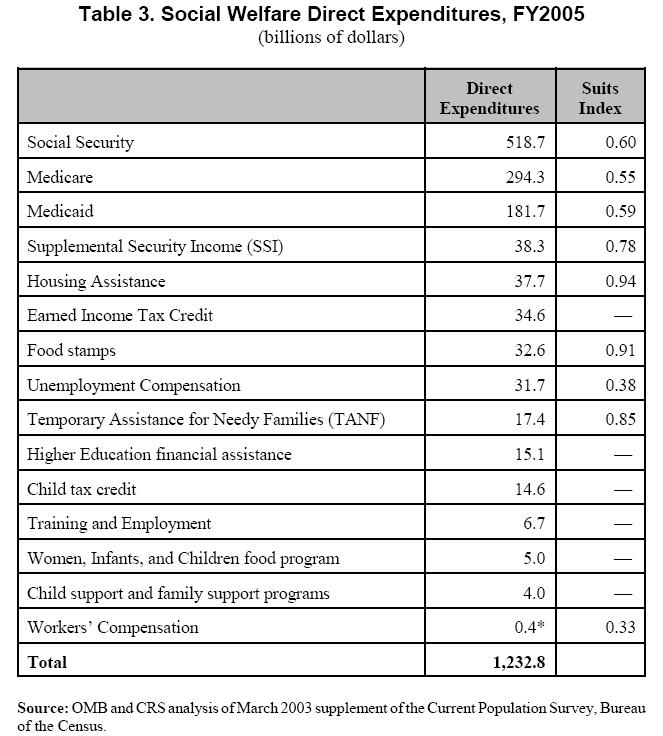

Finally, an examination of two charts in the CRS report are particularly revealing with respect to who benefits from tax expenditures, a point that the TF ignores. Chart 4, below, shows various various tax expenditures and, for each, shows a measure of progressivity, the Suits index. (The Suits progressivity index varies between — 1 (completely regressive) to +1 (completely progressive). The Suits index is negative if the benefits from the program are received predominantly by families in the upper part of the income distribution.)

(Click to enlarge.)

(Click to enlarge.)In other words, the tax expenditures shown are, as a group, not particularly progressive and, in some cases, are downright regressive. In contrast, direct expenditures are fairly progressive:

(Click to enlarge.)

(Click to enlarge.)Taxes are not an unalloyed good. They have undesireable economic side-effects. However, they are, as Justice Holmes reminded us, the price we pay for civilization. The key is not to oppose all taxes, but to design a tax system that maximizes the benefits to the entire society. Part of that design requires that there be progressivity in the tax system, a requirement that the TF consistently ignores.

2 comments:

Deadwieght losses do rise proportionally with the square of the tax rate. That's because DWL is an AREA in the supply and demand diagram, which is a squared amount. That's standard economic theory you'll find in any introductory economics textbook.

But don't take my word for it:

http://www.google.com/search?q=deadweight+loss+square+of+tax+rate

By the way, it has nothing to do with "supply side" economics -- which is not an actual sub-field within economics, and which I don't agree with anyhow.

And recognizing that DWL rises as the square of tax rates does not imply that "tax cuts" always make sense. Instead it shows that by lowering rates and broadening bases, we can make Pareto improvements in the tax system, which is good for everyone. And that's a scientific argument, not an ideological one, as you assume.

It's not at all clear that the relationship of deadweight losses to increases in taxes is all that clear. Thus, in a CBO paper, Recent Literature on Taxable-Income Elasticities pubished in December, 2004, the author states in response to Feldstein's formula for calculating deadweight loss "However, there are exceptions when a breakdown of the response can add insight into the efficiency implications. For example, suppose tax rates rise and, in response, taxable income falls, but a portion of that drop in taxable income is due to increased charitable contributions (and suppose those charities produce positive externalities). Or, suppose that a tax increase is used to finance an underprovided public good. In instances such as those, where external costs or benefits are present, assessing efficiency implications is more complex. (Note: I would have pasted the first part of the footnote, containing the Feldstein formula, however I did not think that it would translate to HTML.)

The point is that governmental expenditures may or may not be like throwing money into a black hole. Where, for instance, government spending is directed to goods that maximize the economy as a whole (the Interstate Highway System,for instance), there is less deadweight. Where the government spending is pure pork (e.g., that part of the Interstate Highway System represented by the Alaskan Highway to Nowhere) Feldstein's formula would certainly tend to operate.

Post a Comment